Wrist and PIN: Why paying from your watch is the future of shopping

How payment tech is coming to your next smartwatch

Cash is the enemy and the tech industry has declared war on your wallet. Forget that contactless card your bank issued you last year, the future of payments are on your wrist, and the likes of Pebble, Apple and Samsung making it happen.

Cash is a burden to carry, cash can be miscounted and you lose your cash if someone steals it. The credit and debit industries are trying to sell convenience, and that’s why there’s been such a push for contactless payments since NFC-chipped cards arrived courtesy of Barclaycard 2008.

Essential reading: Best Wear OS apps

All top smartphones of the day need to be seen with contactless technology on their specs sheets. Google Wallet has been ready to receive over in the US since 2011 and now that Apple Pay has gone live Stateside too, expect to see a lot of mobiles waved at card readers in the close future at an off-license near you.

“What Apple has done is a great thing for contactless overall,” says Mike Saunders, Managing Director of Digital Consumer Payments at Barclaycard. “It will drive a significant improvement in contactless infrastructure in the US. Apple has done a great job of putting that on the map.”

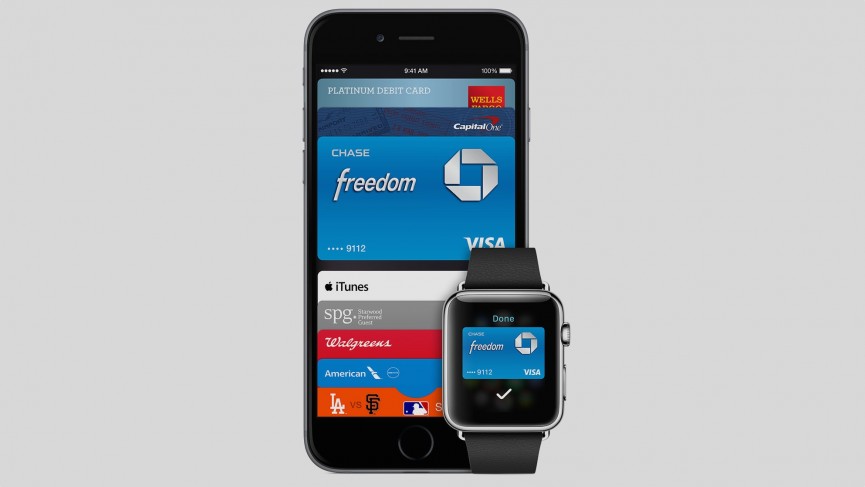

As one of nine issuers partnering Apple Pay, Saunders tells us, straight off the sheet, that “we’re very excited and overall that’s good news” but it feels more like a step back in payment convenience for our money.

Instead of simply getting out a card and tapping it to a reader, you need to pull out a far larger and more expensive device and then authorise it with your fingerprint. The only way to make contactless even more convenient than it already is is by never having to take that card out of your pocket in the first place. And that’s where wearables come in.

Essential reading: Apple Watch review

Barclaycard has been running trials with a system it calls bPay. Currently in the form of a wristband, it’s an NFC chip-carrying device that makes payments just like a card. Wave your arm at the reader and the transaction’s done. It doesn't matter who you’re spending your money though either.

You can attach any UK credit or debit card you like to it – e.g. Visa or Mastercard, or anyone that you bank with – and that’s where the funds will be drawn each time. The idea is that you top-up your bPay account online but you can also set it to do so automatically leaving you free to tap and pay without having to think.

Attendees at the British Summer Time events in Hyde Park and Pride in London got to try out the bPay bands first hand this year. Sadly, there were no specific measurements to determine if wearable payments could cut queue times at festivals, but what Barclaycard did notice was a very high percentage of spend taking place far beyond the dates of the events themselves – a strong indicator that this is way of spending that the public seems to like.

Consequently, Barclaycard has just released a further tranche of 10,000 bPay bands for Londoners to use on the capital’s transport network, instead of Oyster cards, as well as for spending at the usual NFC terminals in shops, cafes, restaurants and all the rest.

A simpler way to pay

“It’s really simple,” revels Saunders. “That’s the ultimate thing. Gone are the days of having to fish in your pocket for something, regardless of what it is, to take the Tube or the bus. We’re eager to see what that does to the behaviour of the people that have the product.”

The beginning of the payment-by-wearable revolution then? Well, quite probably, but the process is not without its barriers to overcome; barriers, fortunately, which Saunders suggests plenty of ways around. The classic issue with wearables, of course, is getting people to wear them in the first place.

“Our early bPay bands are very functional. We’re working on devices that are going to be much smaller, devices that customers can personalise and also devices that will come in different form factors, not just wristbands. On that front, the things that we’re wrestling with are no different to other wearable tech companies.

“We’re working with a range of partners – partners in the fashion space, partners in the sports and arena space - to work our product into things they’re already doing. And then further down the line, as the chip tech evolves and gets smaller, we’re looking at a more ingredient approach, where we’re piggybacking off the work of other tech companies and being an added ingredient in a device that does a lot more. That’s very core to our 2015 strategy.”

Tackling the wearable issues

The key, then, appears to be getting payment technology into the items that we’re already used to wearing. A fashion company is going to be better at creating a beautiful piece of clothing or accessory than a financial organisation. So, payments can bring something even more compelling to garments that we already want. What payments can also do is make an object worth wearing in the first place once bPay and others come up with apps to sit on third party devices.

“The early iterations of smartwatches have had very limited functionality and you still don’t see too many on people’s wrists today,” states Saunders echoing a sentiment expressed by many – tech fans and otherwise.

“Customers want more functionality and they want daily functionality. They also want devices that are comfortable and aesthetically pleasing. If you look at early versions of the smartwatch, they failed some of those tests.

“One of the things that payment does to wearable tech is give it ongoing daily functionality. If you look at fitness bands, the average lifespan is very low. Customers get very excited and motivated to get one. They use it, they’re really into it for the first couple of weeks but, then, after that, the excitement tails off because they’re not seeing anything new in that. You add NFC payment and that’s a device that I’m using five or six times in the day and also getting that great health data from.”

Throw in the increase in NFC infrastructure, hopefully boosted by the likes of Apple Pay, and what begins to take shape is that, in fact, contactless payments could become the single most important driver in the uptake of wearable tech.

Obviously, it’s not all plain sailing. There are still going to be contactless trust issues, whether these transactions are in a wearable form or not. Many people prefer to work in cash alone, some will be concerned by the possibility of racking up debt too quickly and there have been legacy fears over security since the technology was launched.

The last of these is something Saunders dismisses as “customer perception”. The reality remains that the NFC system itself is secure and that using something like bPay offers the same fraud protection guarantee as a credit or debit card, but that might not be something that the average person on the street is willing to listen to.

The other safety measure is that there’s a £20 maximum spend on contactless in the UK at the moment. That’s going up to £30 by late 2015 but it’s going to need to head to £50 and beyond before it becomes part of the weekly shop, one of the cornerstones of customer habits.

Upping the security

The reason that the limit exists in the first place is to avoid huge sums of money getting lost when someone’s pretending to be you, but that’s a space where wearables can help out. Devices like the Bionym Nymi are arriving which can provide a persistent sense of user identity. It’s a wrist-worn device which measures your ECG - a graphical representation of your heartbeat - that’s as individual as fingerprints or retinal eye patterns. The Nymi checks your ID and then keeps you ‘signed in’ until you remove it from your wrist. Once smartwatch and fitness band makers can integrate these kinds of identity biometrics and payment systems, then wearables will have a functionality and convenience that’s impossible to ignore. For Saunders, though, the picture is even bigger.

“The idea of the corporate campus gives you sense of how we’re thinking about this and how it’s really being designed to make someone’s life easier.”

The corporate campus is something that will be trialed at Barclaycard itself. The idea is an NFC-powered wearable that stores company credentials as well as funds. You can use it to buy a coffee on the way to work, to access the lifts, for printing credits, for computer log-in and all the food and drink outlets on site, as well as anything you need outside of work throughout your week.

“In that one example, I was in and out of my pockets about 14 times using three or four different pieces of plastic to do the same thing. Now, before the end of the calendar year, I will never touch my pockets through the day, and that will be a great experience.”

The company that’s taken this concept and run the furthest with it so far is Disney with the MagicBand. After a $1bn investment in the program, visitors to the Florida kingdom can enter the various theme and water parks, check in with fast queue privileges, buy food and drink, unlock their hotel rooms, enter competitions and pick up all the photos of their stay. It’s the complete solution through wearable tech.

So, is paying with your wearable the big money future? Most certainly. It’s a big money present unveiling as we write, with an infrastructure at tipping point. There are huge brands behind it and the interests of the financial sector powering it all the way. As the generations of people for whom cash is the only way begin to dwindle, contactless can only be king. And it’ll pull wearable tech along with it.